A Tale of Two Cities revisited

International relations have entered the theatre of anti-money laundering policy. Sanctions evasion, terrorist financing, tax evasion and the laundering of the profits of criminal enterprises, especially fraudsters and financial criminals, are different phenomena and are not appropriate for a one size fits all approach. Investigators are having too many tasks thrown at them without adequate resources following. Policing has never been adequately resourced and perhaps in a democracy never should be. Policing the market is anathema to the neoliberals that purport to be followers of Milton Friedman, but maybe it is time they actually read the words of their guru:

“I used to be asked a lot: ‘What do these ex-communist states have to do in order to become market economies?’ And I used to say: ‘You can describe that in three words: privatize, privatize, privatize.’ But, I was wrong. That wasn’t enough. The example of Russia shows that. Russia privatized but in a way that created private monopolies-private centralized economic controls that replaced government’s centralized controls. It turns out that the rule of law is probably more basic than privatization. Privatization is meaningless if you don’t have the rule of law.”

Today, it is not just the Russians who have to privatise. It has also become the gospel of the OECD. But no global institution is driving the rule of law alongside or ahead of privatisation. In fact, the political class in power is attacking the impartiality of judges and thus the courts themselves. The new authoritarianism is turning Aristotle upside down as we return to the rule of demagogues and undermine the rule of laws. The new privatisation is creating private monopolies and oligarchs even in relatively new economic areas. They can choose where to headquarter their companies and even the jurisdiction of which they will be citizens. Those choices thus include where and whether they pay their taxes. The once exclusive club of Westerners has been joined by Chinese, Russian, Indian and even other unknown oligarchs. They laugh at sanctions. Sanctions are a badge of honour, just as an antisocial behaviour order is for a juvenile gang member.

As we know, we have no international criminal law, no accepted courts and no enforcement agencies. We have a network of investigators, and again, it is a matter of international relations. The Treaty of Vienna gives diplomats extraterritorial status, and the Treaty of Naples does the same for customs officers. We need a new Treaty, defining a series of predicate offences and giving a designated category of investigator, prosecutor supervised, of course, extraterritorial status to follow the money. We have a model in embryo in Europol and Eurojust. Europol has no policing powers but can facilitate and support a joint investigative team to investigate, and Eurojust can provide legal support, identifying legal problems and discussing legal solutions. Oh, sorry, I forgot. That is why the UK is leaving the European Union with effect from 1 January. Do not mention Brexit!

It is crazy that organised criminality not only finds borders no obstacle but actually profits from their existence. They are an obstacle only to prosecutors and investigators. Cyberspace takes this actuality even further. The money is moving through an imaginary void and is there to be stolen by cybercriminals. How could cyberplod patrol cyberspace? The answer is, of course, by networking in a manner similar to criminal networks. But there needs to be a legal basis for this. COVID-19 by accelerating the process of driving shopping and banking online has increased the urgency for this.

Sanctions on wealthy individuals are not going to work. Dealing with actions by other states of which you do not approve is a political matter, as is terrorism. These matters can only be solved by changes in policy and by negotiation. Police work and even military action can only buy time for politicians to change their approach. The world is changing. The super-rich are getting richer and thus more powerful, the age of the US unipolarity is passing, and governments around the world are becoming increasingly indebted. At the end of the Napoleonic Wars, the great powers created the Congress system, sitting down together every four years to agree a list of problems and see if they could sort any of them out. We are coming to the end of a period of war, and we need a new system to resolve conflicts other than overthrowing governments by force. Then maybe we can turn against organised criminality and get to grips with its money laundering techniques. Until then, it will take advantage of cracks in the existing system. It is rubbing its hands at the prospect of the bill for COVID-19. Cash flow is going to be a major problem, and the drug dealer, the people trafficker and the cyberfraudster have that cash. We need to tighten our definition of money laundering once again to make investigation feasible and concentrate on contract enforcement in this age of cross-border cyber trading. It would be “a far far better thing than I (we) have ever done […]”.

originally published in teh Journal of Money Laundering Control https://www.emerald.com/insight/content/doi/10.1108/JMLC-01-2021-145/full/html

Mind the Gap: troubled implementation of the Prevent Duty at UK Universities

James Maxia, Eva Thomann and Jörn Ege find that there is a considerable implementation gap at UK universities of the ‘Prevent Duty’ introduced under the 2015 Counter-Terrorism and Security Act wherein university lecturers are legally required to identify and report any student they suspect may be undergoing a process of radicalisation. The results of a nationally representative survey suggest the Prevent Duty faces a severe acceptance problem at the frontline. Many lecturers find it difficult to reconcile the role that the Prevent Duty should play in their daily work with what they conceive to be their core professional values and tasks.

In September 2017, a teenager from Surrey, Ahmed Hassan, attempted to detonate a homemade explosive device during a failed terrorist attack on the London underground. In the aftermath of this incident, details surrounding the perpetrator’s participation in the government’s deradicalisation programme – Prevent – in the months prior to the attack prompted further public scrutiny towards the policy. In 2015, the UK government had enacted the Counterterrorism and Security Act, which introduced a statutory requirement for professionals working for education and healthcare institutions to undergo training in recognising signs of radicalisation and a requirement report anyone they suspect of being radicalised. The 2017 incident fuelled existing concerns and contributed towards casting doubt on Prevent’s overall effectiveness and legitimacy. Several vocational and societal groups have expressed strong opposition to the Prevent policy, arguing that it clashes with professional norms of confidentiality and encourages limitations on freedom of expression and discriminatory profiling. In 2016, a group of lecturers from the University of Manchester published a letter detailing their opposition to the policy and voicing concern for “the role of the lecturer, the sanctity of academic freedoms and intellectual curiosity” as well as the undermining of diversity on campus. These concerns were further echoed when in 2019 a judicial review of the Prevent Duty guidance issued to universities by the government found it to be in violation of free speech.

The Prevent policy was originally conceived in 2003 as part of the broader UK counterterrorism strategy (CONTEST) which is predicated on four main objectives: prepare for attacks, protect potential targets while pursuing and preventing terrorist activity (Ibid). The success of the Prevent strand rests on the ability to identify (potentially) radicalised individuals. While the Prevent Duty applies to a range of institutions, one important locus for its implementation are universities, where young individuals make key formative experiences. Among those newly tasked with implementing this duty are university lecturers, who are legally required to report any personal or classroom interactions that may indicate a student undergoing a process of radicalisation.

At first glance it may seem counter-intuitive to engage University lecturers, who have spent most of their careers doing research and teaching academic subjects most of which are unrelated to terrorism, in preventing radicalisation. However, the Prevent Duty is just one example of an ever-growing trend toward “new modes of governance” that involve actors from the private and voluntary sectors into the delivery of public policy. These actors are typically deemed to be in a unique position to help reach the policy goals (here: preventing radicalisation) better than any governmental actor could do it. University lecturers, for instance, interact regularly with students and, particularly in the social sciences and humanities, discuss topics with them that touch upon societal and political issues. They should thus be the first to notice if individual students appear to “go astray”. Asking them to report such individuals seems much more efficient and effective than sending police officers or social workers to campuses to look out for such individuals. What makes the Prevent Duty special, however, is its uniquely politically sensitive and contested nature. As the above mentioned events illustrate, not only its effectiveness, but indeed also its legitimacy are being questioned. But what do we really know about how Uk lecturers think, feel and act when implementing the Prevent Duty in their daily work?

Methodology

In our ongoing study, which has received ethics approval from the University of Exeter, we focus on the role of lecturers in implementing the Prevent Duty. We performed an anonymous online survey in November 2020, to which we invited all lecturers currently teaching at a Social Science or Humanities department at a UK university. We received 1005 responses of which 84.68 percent have a permanent contract at a UK university that involves some form of student contact. Our survey had three main goals. On the one hand, we sought to obtain information about the extent to which UK lecturers are informed about the Prevent Duty, and have made concrete experiences with its application. On the other hand, we confronted lecturers with a fictitious scenario of a student contact to get an impression of their willingness to actually implement the Prevent Duty the way it is intended. Finally, the survey helped us to learn about the attitudes of lecturers toward the policy.

Is the prevent duty effectively implemented at UK universities?

The good news first: the vast majority—86.34 percent—of the respondents have heard about the prevent duty. Moreover, the majority—59.08 percent—are at least somewhat familiar with the Prevent Duty regulations for UK universities. However, a surprisingly large percentage of the lecturers (62.41 percent) report to never have received training on the Prevent Duty. Most of those who do report having received training describe it as being “self-guided material provided by the university” (66.93 percent), as opposed to actual workshops or meetings. We further asked lecturers whether they have ever been in a situation where they believed the Prevent Duty could have been applicable. Only 14.98 per cent indicated this to be the case once or several times. These numbers suggest that (potential) student radicalisation indicating action under the Prevent Duty is a rare event in lecturers’ professional practice. Moreover, many lecturers appear to be only superficially aware of what concretely they are expected to do under the Prevent Duty.

In order to nevertheless gain a robust picture of potential compliance with the Prevent Duty, we also presented the lecturers with a fictitious scenario that, according to the rules, clearly represents a case that needs to be reported, as follows:

“You are having a conversation with a student of yours. The student tells you they have been browsing on a website of a group that is known for its approval of the use of violence or of illegal means, which it sees as unavoidable for changing the existing societal order. The student expresses sympathy with the philosophy of the group and the readings promoted on that website, and speaks about the need to get involved in the cause.”

For various subgroups we then specified either the nature of the threat (right-wing extremism or Islamism) and the closeness of the mentoring relationship.

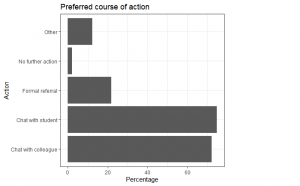

Figure 1: preferred course of action after being exposed to fictitious student contact scenario (multiple answers possible; N=809)

After being presented with this scenario, the majority (78.86 per cent) find the student’s behavior somewhat or very concerning both to their own safety and that of others. Nevertheless, less than half (33.37 percent) consider themselves likely to report the student under the Prevent Duty. As Figure 1 shows, only about 21.76 percent would formally refer the student. Instead, lecturers’ preferred options are to seek advice from colleagues (72.18 percent) or, mainly, to speak to the student privately (74.78 percent). There appear to be significant barriers to an effective implementation of the Prevent Duty at UK universities.

What role for the Prevent Duty in lecturers’ daily work?

Most of the lecturers we surveyed do not see the implementation of the Prevent Duty as a major priority in their daily work (89.74 percent). Instead they prioritize defending academic freedom, delivering high-quality education (91.58 percent), as well as ensuring and delivering equal treatment, opportunity and mentoring to students (93.69 percent). Our survey makes it very clear that lecturers consider these (and to a much lesser degree, contributing towards the University’s ability to compete for students and provide good value for money), to be the essential elements of their daily work. At the same time, the lecturers fear that the Prevent Duty might potentially cause them to compromise on their standards of educating students and defending academic freedom (53.29 percent), providing equal treatment, mentoring and pastoral care to students (55.40 percent).

In contrast, most lecturers agree that being able to act in accordance with their own values, ideological principles and political convictions is a major priority in their daily work. About half of them (45.45 percent) perceive that having to apply the Prevent Duty may cause them to compromise on their political and ideological principles and values. Accordingly, only a relatively small fraction of the surveyed lecturers (17.56 percent) report to be willing to put efforts into implementing the Prevent Duty to achieve its goals. The Prevent Duty, in other words, faces a severe acceptance problem at the frontline.

These results illuminate that even if the training can and should be improved, getting UK lecturers to police and report their own students might be a very difficult or even impossible task. It appears that many lecturers perceive the Prevent Duty to stand at odds with core values and tasks of their own profession. Moreover, the politically sensitive nature of the prevent duty might pose serious obstacle for its implementation. Given that their work requires lecturers to build a relationship of trust with students and defend academic freedom—both of which they perceive to stand at odds with the Prevent Duty—, this implementation gap is unlikely to disappear. Handing over a core state task such as antiterrorism policy to societal actors without considering the compatibility with their existing responsibilities is unlikely to be an effective approach to preventing student radicalisation.

Attitudes to digital contact tracing: citizens do not always prioritise privacy and prefer a centralised NHS system over a decentralised one.

Citizens’ concerns about data privacy may reduce adoption of COVID-19 contact tracing apps, making them less effective. Based on a choice experiment (conjoint experiment), Laszlo Horvath, Susan Banducci, and Oliver James find that citizens do not always prioritise privacy and prefer a centralised NHS system. They also find support for a mixture of contact tracing done digitally with limited human involvement. On the basis of these findings, they argue that the potential for the adoption of such apps in the UK appears high.

The government recently rolled out its contact tracing app in England and Wales. This launch came about after many stops and starts in developing and trialling an app – six months behind Singapore, the first country to adopt an app, and four months behind the first European apps in Italy and France. An element of a successful test and trace system, digital contact tracing relies on mobile applications and wearable technologies to record when users are in close proximity to one another for an extended period of time, and then notify a user if one of their contacts has tested positive for COVID-19. The app launched in England and Wales, which relies on existing Apple and Google technology to record contacts on the handheld device, also includes features where users can scan a QR code to record their location as well as an isolation counter to keep track of the days spent in isolation if needed.

For effective deployment of the new technology, public trust and confidence is key. Initial interpretations of an Oxford study suggested uptake and use would need to be around 60% for a contact tracing app to be successful, although recent estimates clarify that digital contact tracing is successful at much lower rates as well (at 15%) if combined with other interventions. Yet there is more to confidence-building than those initial adoption rates. In the words of an Isle of Wight GP: “My concern when the public […] will feel ‘what’s in it for me’ and be disincentivised. The truth is very little is in it for them other than the greater good,” the BBC quotes.

Our research was motivated by concerns about privacy as a limit to potential for citizen take-up of apps. In fact, using a conjoint experimental design, we found that citizens do not always prioritise privacy but give high preference to a centralised system led by the NHS over a decentralised system such as the one rolled out. This may be related to the strong support for the NHS during the crisis, one manifestation of this having been the nationwide clap for NHS carers, and the perception that the NHS should be part of the solution for the health crisis. Even when we highlighted a salient threat of unauthorised access or data theft, it did not significantly alter respondents’ preferences. We further find that citizens tend to support a mixture of contact tracing done digitally with limited human involvement. On the basis of these findings, the potential for adoption of apps appears high.

Earlier in the summer, and just weeks after our data collection finished, decisionmakers in the UK abandoned the NHS-led centralised system. According to news reports, this had more to do with technical failure than privacy concerns, though earlier the government insisted that the existence of the centralised NHS server improves the process of contact tracing by making audits and system adaptation possible while also minimising the number of low-risk notifications. While decentralised systems, such as the one being rolled out now, are praised for better overall privacy-preserving features, the lack of central oversight does limit human involvement – in practice, however, this is a legislative feature. After the failure of the first tracking app, it is unclear how meaningfully digital contact tracing will be integrated with the other elements of the test and trace process.

Our findings also highlight additional questions about how citizens’ relationship with their public health authorities affects cooperation with initiatives like digital contact tracing. In the UK, a long history of publicly funded, largely free at point of delivery, high-profile healthcare appears to have created the pre-conditions supportive to cooperate with national public health programmes. This opportunity has not so far been sufficiently exploited but could bode well for adoption of the new app system now that it is finally being rolled out for England and Wales.

The initial uptake of the ‘Protect Scotland’ mobile app launched by NHS Scotland earlier in September is consistent with this view, with over one million downloads within the first week. The challenge will be making sure the government keeps its side of the bargain in rapidly testing, quickly turning around results and then, for those who test positive, tracing contact – providing information quickly enough to those who were potentially exposed to the virus to isolate themselves before individuals transmit the infection to others. The app is only intended to improve the efficiency of the latter stage of an effective test and trace system. As the recent estimates indicate, there are significant issues with the first stages.

It is accepted even among those who are developing and promoting a contact tracing app that it is one tool in a comprehensive test and trace programme. Even if the app is enthusiastically downloaded and used by individual if the rest of the test and trace system, including effective and speedy testing and human contact tracing, is not delivering, the initial enthusiasm on the part of citizens to cooperate may wane.

originally posted at https://blogs.lse.ac.uk/politicsandpolicy/uk-attitudes-to-digital-contact-tracing/

No, even this time is not that different COVID-19, the sudden and mysterious death of the SGP and European integration

By Jonathan C. Kamkhaji University of Exeter associate fellow and Polytechnic University of Milan

What if, within a couple of weeks, the term limit for US presidency was removed? What if, within the same couple of weeks, the UK abandoned its signature first-past-the-post and turned to proportional representation? What if, within the same limited amount of time, Italy surrendered perfect bicameralism or France rejected semi-presidentialism? Although these may seem outlandish questions, the magnitude and pace of the change triggered by COVID-19 on economic policy coordination within Economic and Monetary Union (EMU) resembled that of the above hyperboles.

In a nutshell, the European Union (EU), less than a month after the epidemic curve started its raise in Italy in February, simply suspended its much contested and polarizing mechanism for multilateral economic surveillance – the Stability and Growth Pact (SGP).

Literally in the blink of an eye, those rules that seemed to be, if not eternal, at least stable and structural elements of economic policy coordination within the EMU and key to guarantee its stability and trustworthiness vis-à-vis global markets and investors, disappeared. Technically, they were simply put in abeyance not to get in the way of Member States’ countercyclical fiscal expansions. Practically, the set of rules and parameters to which EMU Member States had voluntarily agreed to subscribe in order to deter fiscal profligacy and extreme financial follies since the early 90s have been discretely set aside for an indefinite amount of time – and no mayhem has, as of yet, unfolded in international financial and debt markets. This is even more remarkable if we realize that the suspension of the disciplinarian mechanism took place against a war-like global scenario poised to mark worst global GDP contraction of the last century.

Needless to say, this change is having and will have far-reaching implications for EU economies and economic and political integration, but I think that while these implications are still brewing within the EU (with the establishment of recovery funds and true fiscal solidarity as the main themes) it is more important, for now, to focus on how this sudden stop and reversal of rules for fiscal discipline has materialised. This is because the EU (and we…) live in times of polycrises, that is, crises that are multiple and overlapping, creating thereof polycleavages. Some go as far as arguing that the whole EU decisions and policy making is undergoing a process of crisisification, understood as the normalization of “crisis‐oriented methods for arriving at collective decisions”. What’s remarkable, however, is not simply the accumulation of crises and its influence on EU decision and policy making, but rather the fact that the EU is actually deepening its economic and political integration, not despite the crises, but through the crises.

Then, if crisis mood has become the new normal for the EU, and crises indeed have the potential to deepen integration, the question is how to explain this further quantum leap in terms of existing models and theory of integration. At the outset, we note that the EU, although entangled in and somewhat plagued by its fragmented governance, has a penchant, at least in the economic realm, for spot, landmark political decisions – like the decisions to renege on the no-bailout clause of Maastricht and rescue Greece in 2010, or to reinterpret monetary neutrality and do “whatever it takes” to save the common currency. Interestingly, those landmark decisions, like the one suspending the SGP, were purely political and came with little or no policy attached.

In all of these crises it is only ex post, after the grand political declarations have been fed to the public, that policy commences its engine, crucially surfing on the feedback of the initial declaration effect. A similar dynamic is captured by a number of new models of integration and crisis management. One of such models is failing forward. According to the model, intergovernmental decision making, which typically occurs in times of crisis, systematically leads to incomplete institutional design. The latter stimulates functional spill overs which in turn lead to further crisis. Crises are then faced again by piecemeal intergovernmental decisions which sow the seeds of future crises and failure. As a result, the EU invariably fails forward. Applying the insight of this model to the current crisis may be depressing but in fact we can already see the merits of the failing forward argument when we observe the massive political conflict which unfolded after the decision of suspending the SGP and rethinking the whole fiscal arm (and economic governance) of EMU. Call me a pessimist, but a piecemeal, incomplete integration of fiscal policies is still more likely than the comprehensive reform the EU needs in the fiscal domain. Yet again, a stern political turn in the right direction mitigated by incremental and insufficient policy instrumentation and institutions.

Another model which draws on contested governance and comes to interesting conclusions about crisis management and integration is presented by Jabko in its sociopsychological account of the Eurozone crisis of 2010-2013. This contribution points to the highly guarded boundaries of policy paradigms to show how decisions taken under conditions of extreme uncertainty (typical of crises) defy paradigmatic expectations and conform instead to malleable repertoires. As crisis decision making is constrained by material and cognitive limitations, the resort to rigid blueprints for action like paradigms takes place post hoc, in the policy phase, but is hardly observable in the context of the single decision which triggers the whole process of change. Yet again, this argument may lead to bitter conclusions. If suspending the SGP may have been a correct decision pushed by the acuteness of the crisis, and defying more than 20 years of ordoliberal paradigm, the construction of institutions and policy around this decision may bring us back, again, to an incomplete design of fiscal integration.

The last model which may explain the sudden and mysterious death of the SGP is contingent learning. According to this model, in episodes crisis management characterized by stress, uncertainty, time pressure and demands for rapid action, real-time policy change takes place through associative processes of contingent learning and the nature and scope of this behavioural change is greater than re-design and incremental adaptations. In change-or-die situations we find accidental heroes. They produce significant change and only later they reflect on ‘what have we done’ and start drawing inferences from experience, thus entering the world of classical policy learning – and policy making. If we stick to this model, we have then to hope for an ex post learning process which does not go back to the tenets of the old paradigms once the storm has been cushioned.

In any case, even this time does not seem to be different: existential threats provide the potential to lead in the right direction, but a little recovery may be enough to stick to the old, failing principles and decisional traps.

The impact of Brexit on Justice and Home Affairs (JHA) cooperation and safety and security in the UK and the European Union

Bill Tupman, Honorary Fellow, Centre for European Governance, University of Exeter

June 25, 2020

As Brexit approaches one of many questions is, what will its impact be on Justice and Home Affairs (JHA) cooperation and consequently on safety and security in the UK and the European Union? An unanticipated but related question is: what will the impact of Covid-19 be on the way crime is organised and hence on JHA?

The UK has always been an outlier in European Justice and Home Affairs policy. The adversarial system, the absence of judicial supervision of investigation, trial by jury and the Common Law system were the main obstacles to cooperation between England and Wales (but not Scotland which has a procuratorial system) and the police and courts in the rest of Europe, with the possible exception of Ireland. The ability and skill of UK detectives were admired as was the bottom-up nature of British policing: including high discretion of the individual police officer, absence of a direct entry officer force, unarmed policing, service policing, absence of political control and consequently policing without fear and favour. The stability of the British legal system was much admired, too, although this stability has been absent in recent years with constant legislative change in investigative and criminal law. In contrast the rest of the European Union followed Napoleonic models and what has been referred to as a Civil Law system, although, in fact there were and are two competing systems of judicial supervision: judge-led and prosecutor-led.

Justice and Home Affairs cooperation began as a response to a perceived threat from organised crime terrorism and immigration to stability and prosperity in the EU after the removal of the internal borders, assumed to be an inevitable consequence of the Single European Act. The first response was the Schengen Convention, but in the codicils to the treaty of Maastricht there was also a paper on the use of information technology to counter these problems. From this latter grew a series of databases, initially conceived as a way of facilitating police cooperation by abolishing jurisdictional borders by the use of cyberspace.

So post-Brexit, the possibility is that the UK becomes an offshore haven for transnational criminal actors, because extradition will be problematic, money-laundering will be easy and cooperation will be one way…The UK will expect cooperation from the rest of Europe in finding and returning its offenders from Europe, while refusing or delaying the extradition and provision of evidence to police and judicial authorities outside its borders. It also becomes attractive to people-smugglers as its stronger border controls will enable them to put their prices up. Criminal networks will change behaviour wherever they see opportunities for extra profits and lower likelihood of prosecution.

Criminal networks have had to change their modus operandi as a result of Covid-19. Fewer flights, ferry movements and movement in general make drug trafficking and people trafficking mire exposed to discovery by the security services. On the other hand, there are new opportunities: black markets in PPE, counterfeit medicines, snake oil salespersons, and fraudulent health products are obvious opportunities. So are personnel shortages in health services. Illicit drugs have already been discovered in consignments of PPE. The movement to commit crime via the internet will be further enhanced. Intelligence about the changing nature of criminality was always important, but the pace of change is on the increase. When Romanians are sent to Ireland to open bank accounts into which victims make payments for the purchase of non-existent goods, it is likely that they are doing the same in other countries and investigators need to know this as a matter of urgency.

Nonetheless, there is confidence on the UK side that there will be cooperation under the banner of Mutual Legal Aid agreements that will lead to the arrest and prosecution of criminals, but such confidence appears to underestimate the nature and complexity of cross-border criminal networks as well as their changing modus operandi. UK investigators and politicians, however favour disruption over prosecution, arguing that prosecution takes too long and that juries tend not to understand complex cases and therefore acquit. This may reflect a flaw in the adversarial system, however and further enhance the possibility of the UK becoming the refuge of choice for both criminal money and illicit venture capitalists.

If there is lack of reciprocity, there is a likelihood that Continental investigators will give UK requests for assistance a low priority. Requests via Interpol for information are unlikely to run as smoothly as European Arrest Warrants and European Information Orders unless there is to be significant UK investment in technology and personnel into Interpol. The Swedish Decision, for example, lays down an 8 hour turnaround time for urgent requests for intelligence and/or information, tapering to one week or even two in less urgent cases.

The present author, when fortunate enough to be invited to act as the UK “expert” on a project investigating the possibility of a single database in the EU for prosecutions of criminal offences, interviewed two members of the then NCIS . When asked what would be the top of a UK investigators’ shopping list, the answer was “data-sharing”. In other words a legal basis for sharing data between investigators in different countries. The Prüm Decision and, to an extent, the Swedish Decision, provided for this, but UK politicians are uncomfortable with it, partly because of supervision by the ECJ, but partly because though they might be happy to look at data from EU countries, they are much less happy to have investigators from those counties accessing UK data. The EU itself is, of course, very suspicious of UK data protection law and procedures. That the Home Office failed to admit the wrongful storage of data from EU databases and its sharing of such data with the US and probably the rest of the “Five Eyes” has strengthened this suspicion and made access to the Schengen database in particular unlikely after Brexit.

The Schengen Database enables border control cooperation, law enforcement cooperation and vehicle registration cooperation. At the end of 2017 it had 76 million records, it was accessed 5.2 billion times and recorded 243,818 hits ie searches that created an alert and the appropriate authorities agreed. In March 2018, exchange of fingerprint data was enabled. At the end of 2021 it will also be capable of sharing of biometric information, for example on missing persons, alerts on vulnerable persons, information on persons suspected of involvement in terrorism-related activities, bans on entry and other aspects of illegal immigration, plus extend alerts on other criminal activities. It will also provide enhanced access for other EU agencies. Exclusion from the database will increase response time for UK requests for intelligence and access to alerts on individuals.

The UK is already excluded from access to the Schengen information System for immigration alerts as it is not a member of Schengen. There are also databases run by Europol, along with the system of Joint Investigative Teams. The UK is likely to be able to negotiate access to SIENA, the Secure Information Network Exchange Application, as the USA and Australia have already successfully negotiated such access. It has nowhere near the capabilities of the Schengen Information System but is extending its activities. It should be possible for the UK to participate in joint investigative Teams as third countries may be invited to join a particular case, but, of course, subject to judicial supervision under the law of the lead country. It is unlikely that the UK would be allowed to lead a Joint Investigative Team, but the final agreement has not yet been negotiated. There is still an assumption that somehow the UK is superior in investigative skills, but as already noted, its record on fraud and financial investigations is not seen that way by the rest of the European Union.

It should not be forgotten that there are plusses for the EU in the departure of the UK from the JHA system. For example, will remove the last major obstacle to the establishment of a European Public Prosecutor, with the power to supervise cross-border investigation within the EU and bring prosecutions in appropriate national courts. Working alongside Eurojust, such an office should be able to tackle the problems of preserving the chain of evidence across judicial boundaries, identifying jurisdictional problems and further the process of creating European Criminal Law, perhaps even the Corpus Juris already proposed for prosecuting fraud against the European Budget, but more likely through a series of framework agreements and directives such as the Anti-Money Laundering Directives.

If there is one certainty, it is that police officers will always find a way to work together and that politicians will have to legislate to legalise their operation if it leads to successful interdictions of criminal networks. A Dutch Chief constable told me back in the 1980s that Schengen became necessary when Dutch cranial investigators were found to be operating south of Paris in pursuit of a drug trafficking operation. Information and intelligence will always be exchanged informally. The problem is turning such exchanges into evidence that can be used in Court, which is why justice and Home Affairs policy exists.

A reflection and a warning – Universal Support

Universal Support.

Christos Kotsogiannis, Professor of Economics, University of Exeter, and Director of the Tax Administration Research Centre (TARC).

March 26, 2020

Who would expect this three months ago? Certainly, we did not even know that such virus existed! Now the world is facing an ‘invisible enemy’ which has (putting the health crisis and the immediate need to respond to this aside!) disrupted economies and society on the scale that most of us have never witnessed, seeking ways to fight against it. Many countries have taken extraordinary fiscal and monetary policy measures, announcing a plethora of unprecedented fiscal stimulus packages to smooth out consumers’ income and stimulate demand and limit the human and economic impact of COVID-19.

Already significant global production has been lost, and the forecasts for growth are being continuously revised, downwards, as events further develop.No matter how optimistic one is, the current pandemic crisis will inevitably lead to a deep economic crisis with long lasting impact (than the economic crisis of 2008). The sheer magnitude of the pandemic shock makes forecasting incredibly complex. The extent of the lost production will of course depend on how severe and persistent the pandemic is, as well as the measures countries adopt individually and collectively. Stimulating demand, as desirable as it is, will not be enough as the global supply chain is also disrupted (even if consumers’ purchasing power does not change, demand cannot be fulfilled if the global supply side is severely affected by the necessary lockdown).

A crisis of this magnitude requires bold actions. A combination of direct transfers to consumers and support (direct and indirect including deferral of payment of tax liabilities) to businesses is likely to be an effective policy – but getting the mix right for the latter is challenging and will depend on administrative capacity. Delivering brand new administrative systems to administer complex policies is hard, as is to set income and profits thresholds for which assistance policies may depend upon. How much and how quickly resources can get to households and business is therefore a pressing issue. If financial support is difficult to deliver in a timely fashion universal support is the right instrument, even though some ‘non-deserving’ businesses might benefit from them too.

The pandemic is affecting supply, and productivity, of the economy and as such will make business investment more costly. A change also in the way we do things is required. Social-distancing and lockdown policies mean working from home, for those sectors that can. But working from home has its own limitations, and adjusting to this is not only challenging but takes also considerable time. If aggressive demand-boosting policies are not adopted, the incentive of business to invest will be reduced further fuelling a loss in productivity which in turn will fuel even less demand. If not acting decisively, there is a danger that economies will find themselves locked in a ‘low-economic-growth-trap’.

Importantly, to win the ‘war’ against the ‘invisible enemy’ global coordination is needed, as the pandemic is affecting the global economic network. Though there are good signs of this happening already, more needs to be done. We live in unprecedented times, but this is the time where the global community should realise that it is better to coordinate than to compete. This, inevitably might help the global community in solving another big challenge it faces, for example, climate change. When normality resumes, the pandemic experience should make climate change coordination easier to achieve. While the 2008 crisis was more of a crisis of institutions the 2020 COVID-19 pandemic is not. Importantly, the ‘shock’ is symmetric and affects all countries. But how successfully a country deals with the pandemic will depend upon how quickly the institutions have been mobilised. This realisation, and the successful conclusion of the pandemic, can act as a ‘coordination device’ where we consumers, producers, states and international organizations coordinate on a good equilibrium following the social norms consistent with the common good. This might take time but there is hope that for a much better world after we get through this.

Conservative Party divisions contributed to the failure of Brexit negotiations, new study shows

By Claire Dunlop, Scott James and Claudio Radaelli.

Divisions in the Conservative Party allowed the European Union to set the agenda during Brexit negotiations, a new study shows.

The EU was able to monopolise the production of key negotiating texts and guidelines because the Tories were distracted by infighting, the evidence collected by academics says. This allowed the EU to “box-in” the UK. As a result, UK negotiators have been forced into a series of incremental and last-minute concessions.

Researchers from King’s College, University College London and the University of Exeter tracked key Brexit decisions and developments by the UK government between June 2016 and May 2019. Claire Dunlop, Scott James and Claudio Radaelli analysed public documents – Brexit documents and planning, civil service reports about Brexit, reports by think tanks reports and media coverage over this period. They interviewed seven UK policy makers and external policy stakeholders – from thinktanks, business, trade associations, lobbyists in the summer of 2017 and 2018.

The study suggests the path towards Britain leaving the EU would have been smoother if Theresa May and her ministers had listened more to experts, and the public, so there could have been genuine learning process about a new deal and what it would involve.

Professor Claire Dunlop, from the University of Exeter, said: “Of course Parliamentary arithmetic has made the Brexit process complicated, but a bigger problem has been that the Government’s failure to find effective ways to listen and learn has created ping pong, not debate which can solve problems.”

The study, published in the Journal of European Public Policy, shows British negotiators were restricted to having to bargain because of Conservative Party instability following the June 2017 election. The Government had to prioritise its survival and the management of the Conservative party, instead of long-term strategic policy thinking about Brexit.

This helped to make Britain’s exit from Europe an intractable policy issue, but ministers didn’t try to find new ideas or policy to end this impasse because of a culture of mistrust and suspicion generated by the referendum and cabinet splits. Instead they created mistrust by not communicating with each other, meaning different government departments were sending conflicting messages.

Professor Claudio Radaelli, from UCL/School of Public Policy, said: “Even before the 2017 election Theresa May was almost impermeable to arguments aired in cabinet, and instead relied on a small and narrow clique of Eurosceptic MPs to formulate her early Brexit ‘strategy’. She felt as if she had to do that because she had lost her majority.

“She thought asserting control over the process was best because of splits in her party, but instead of solving problems this caused confusion.”

The research describes a bunker-mentality in No.10, where the Prime Minister and staff tried to use obfuscation to deflect challenges. This position was untenable, however, once the UK triggered Article 50 in March 2017 and the Brexit negotiations got underway. The lines of responsibility were blurred by the fact that the UK’s lead official negotiator, Oliver Robbins, originally had a dual reporting line to the Brexit Secretary and Prime Minister. This created tensions with No.10. His move to the Cabinet Office in September 2017 undermined the position of DExEU, contributing to its high turnover of ministers and senior officials and eroding its capacity for institutional memory and accumulation of expertise over time.

Overall the Brexit process travelled in a “highly dysfunctional form” that “prioritised short-term political demands (namely, government survival and party management) over long-term strategic policy thinking”.

The study is fully accessible in gold open access at:

https://www.tandfonline.com/doi/full/10.1080/13501763.2019.1667415

Regulating Financial Technology – Professor Alison Harcourt

Originally appeared in Risk and Regulation: http://www.lse.ac.uk/accounting/assets/CARR/documents/R-R/2019-Summer/190701-riskregulation-05.pdf

Financial technology (FinTech) is greatly changing the way in which citizens live and work on a day to day basis. Fintech refers to technological solutions for electronic transactions such as blockchains, cryptochains, digital currencies and peer-to-peer online lending. The introduction of cryptocurrencies around the globe, such as Altcoin, Bitcoin, LiteCoin, PeerCoin and Ripple, and the adoption of national e-currencies, such as the Bank of England’s RSCoin and the M-Pesa in Kenya, are accelerating FinTech use. The growth in mobile phone use, interfaces such as Alexa and Google Home Fiber Voice and social media platforms ease the payment of online goods and services.

As the world moves towards paperless money and online transactions, London has established itself as a world hub for FinTech. The UK’s FinTech was worth £6.6 billion with an annual growth rate of 22 per cent between 2014 and 2016 accord – ing to HM Treasury (2018). The greatest bulk of this income is from cryptocurrency transactions and peer-to-peer lending. UK Trade & Investment (UKTI) estimates the highest growth to be in ‘peer-to-peer lending, online payments and the data and analytics products (credit reference, capital markets and insurance)’ which represent 60 per cent of the market. In its 2018 FinTech strategy, the UK Treasury stated ‘the UK market is one of the most attractive markets in Europe based on our analysis of market opportunity, availability of capital and regulatory environment’. With more people working in Fintech in the UK than in New York, Singapore, Hong Kong and Japan combined, the UK market has become an important part of the global economy. In face of these developments, regulatory responses have invariably been characterized as a game of catch-up. At the same time, regulatory responses have also been strategic, involving processes both of regulatory competition and cooperation.

The overall regulatory goal has been to encourage solutions and new market players to FinTech with the support of government measures. The UK has been particularly proactive. This began in the UK when the Financial Conduct Authority (FCA) was looking for innovative ways to move the UK out of the financial crisis and at the same time to reform and regulate a changing financial sector. The FCA established Project Innovate, ‘regulatory sandboxes’ and its FinTech Initiative. The sandbox schemes waived a series of FCA rules for a small number of FinTech start-ups. This was to create a ‘safe space’ for company innovation where companies could test new goods, services and delivery mechanisms. The idea was not new but was based on ‘Innovation Deals’, such as the Green Deal programme of the Netherlands. Such programmes ‘do not support “normal” business activities, but would be restricted to innovative initiatives that have only a recent and limited or even no access to the market with the potential of wide applicability’ (European Commission, 2016).

The first FCA sandbox in 2016 fostered 24 companies.1 By 2018, it had reached its fourth cohort with 29 companies. 2 This attracted new start-ups to the UK such as SETL which worked in the retail sector as the first company to use a digital ledger. At the time of writing, the FCA was running ‘Tech Sprints’, assist – ing companies to innovate on the regulatory front. In 2018, the FCA was also running Innovate Finance events in conjunction with the Treasury and the Department of International Trade.

The UK sandboxes triggered interest from the European Com – mission and states around Europe. FinTech sandboxes have begun to emerge in Denmark, Germany, Ireland, Netherlands and Sweden. Globally, this was followed by regulatory sand – boxes being set up in Hong Kong, Australia and Singapore.

Other UK-led initiatives have since been noted such as the relaxation and introduction of flexible rules for selected new market entrants and the introduction of self-regulatory trust schemes. These include FinTech developments by the US Federal Reserve Board, US Treasury and Securities and Exchange Commission (SEC) and the incoming US financial law which raises the Dodd-Frank threshold from $50 billion to $250 billion for smaller enterprises and eases restrictions for FinTech (Thomas, 2018). Trust schemes include the European Union’s eIDAS Regulation on electronic identification and trust services for electronic transactions in the internal market which came into effect in 2016. In the US, regulatory guidance has accompanied the legality of cryptocurrencies via the Financial Crimes Enforcement (FinCEN) agency and the Internal Revenue Service requirement that intermediaries have to clear with them prior to establishment (IRS, 2018).

In the UK, FinTech was also seized upon for the establishment of new trade relations. Cross national cooperation with the FCA involved, for example, setting up RegTech partnerships with Australia and Singapore in 2017. In 2018, FinTech was a key highlight of UK trade negotiations with India where the two partners aimed to ‘deepen bilateral collaboration on Fin – Tech and explore the possibility of a regulatory cooperation agreement’ (Joint statement UK-India, 2017) including the establishment of a ‘FinTech Bridge’ between respective regulatory authorities. Indian and African states are of particular interest to the UK given the growth in FinTech. Citizens, particularly in rural areas, have limited access to banks and normally financial transactions are done via post offices and other local intermediaries which incur time and fees (World Bank, 2017). Mobile phones are rapidly alleviating this problem with applications and online bank accounts which increase financial inclusion of citizens in the economy.

FinTech presents many advantages particularly as it substantially lowers the cost for transactions in comparison to fiat money. However, the pace of technological change also presents many challenges. Financial services have for decades been operated by established incumbents (banks and intermediaries) with cultures that often slowed technological adoption and barred entry for new operators. Similarly, technological solutions are developed by the largest tech companies worldwide presenting problems of market concentration, customer lock in and lack of interoperability. Lastly, the need for customer authentication often requires technologies such as device fingerprinting, voice and facial recognition as well as biometric data which is increasingly used to authenticate identity. For example, India has introduced the AADHAR card which has registered biometric data (including iris scans and thumb prints) of over 1.2 billion people. The creation of huge databases presents not only vast opportunities for FinTech on many fronts but also challenges to security and privacy. International payments also encounter cross-border problems of data localization and passporting.

The UK however is clearly acting as policy entrepreneur in steering the future trajectory of FinTech development and how this game at regulatory competition will eventually develop, what trajectories will become critical, and how regulators will be positioning themselves in FinTech represents one of the key regulation research agendas over the coming years.

1 Billion, BitX, Blink Innovation Limited, Bud, Citizens Ad – vice, Epephyte, Govcoin Limited, HSBC, Issufy, Lloyds Banking Group, Nextday Property Limited, Nivaura, Otono – mos, Oval, SETL, Tradle, Tramonex and Swave.

2 BlockEx, Capexmove, Chasing Returns, Community First Credit Union, Creativity Software, CreditSCRIPT, Dashly, Ehterisc, Finequia, Fractal, Globacap, Hub85, London Me – dia Exchange, Mettle, Mortgage Kart, Multiply, Natwest, NorthRow, Pluto, Salary Finance, TokenMarket, Tokencard, Universal Tokens, Veridu Labs, World Reserve Trust, Zip – pen, 1825, 20|30.

REFERENCES

Arner, D.W., Barberis, J. and Buckey, R.P. (2017) ‘FinTech, RegTech, and the reconceptualization of Financial Regulation’, Northwestern Journal of International Law & Business 37 (3) (Summer 2017): 371–413.

European Commission (2016) ‘Better regulations for innovation-driven investment at EU level’, Directorate-General for Research and Innovation. https://publications.europa.eu/ en/publication-detail/-/publication/404b82db-d08b-11e5-a4 b5-01aa75ed71a1/language-en/format-PDF/source-79728021 (Accessed 24 May 2019).

HM Treasury (2018) Fintech sector strategy: securing the future of UK Fintech. https://assets.publishing.service.gov. uk/government/uploads/system/uploads/attachment_data/ file/692874/Fintech_Sector_Strategy_print.pdf (Accessed 21 March 2019).

Internal Revenue Services (2018) Internal Revenue Bulletin. Notice 2014-21. https://www.irs.gov/pub/irs-drop/n-14-21.pdf (Accessed 21 March 2019).

Joint statement by the Chancellor of the Exchequer and the Finance Minister of India at the 9th UK-India Economic and Financial Dialogue, Delhi, 4 April 2017.

Thomas, L.G. (2018) ‘The case for a federal regulatory sandbox for Fintech companies’, North Carolina Banking Institute 22: 257–82.

Farmer-centred innovation and knowledge exchange at the ESEE 2019

Beth Dooley is a second-year PhD student with the Centre for Rural Policy Research in the Sociology, Philosophy, and Anthropology Department. She received the Rowan Johnstone PhD Studentship to explore the myriad complexities involved with building resilience in UK agricultural policy.

Thanks to funding from the Centre for European Governance, I had the privilege of attending the 24th European Seminar on Extension (and) Education, or the ESEE 2019, from the 18-21 June 2019 in Acireale, Italy, positioned along the eastern coast north of the city of Catania, Sicily. As an agricultural lawyer specialising in farm succession planning, rural development, sustainable agriculture and mediation, I’m now broadening my skill set to include farmer learning and knowledge exchange as a rural sociologist by undertaking a PhD at the University of Exeter. Therefore, this conference was incredibly important to attend as the hub for the leading academics and practitioners working on agricultural knowledge exchange and innovation processes to highlight advances in research, practical implementation experiences, outcomes, benefits, challenges and next steps. Conference delegates came from all over Europe and beyond (Iran, New Zealand, US, etc.) to engage with issues around innovation throughout agriculture and the policy and governance structures that enable those processes to flourish. Key questions explored throughout the conference that I need to critically engage with for my PhD research and beyond in this field are the role of facilitation, farmer learning evaluation, complex decision making skills and capacity development, and how programmes, projects and initiatives value the targeted stakeholders’ input in designing the intervention meant to contribute to some type of change and learning, as well as how they facilitate the design of innovation support services to incorporate that approach.

The opening keynote address ‘Transformation, Disruption and Plurality in Agrifood Systems: Emerging Directions for Research on Extension’ was delivered by Dr. Laurens Klerkx of Wageningen University, challenging the delegation to think critically about future questions to explore how we understand and facilitate agricultural knowledge exchange and innovation processes.

Amongst many incredibly important areas identified in relation to policy and governance frameworks, he pointed to the inherent contradiction between the push for co-creation in agricultural research for innovation and the way current funding structures work. Co-creation involves research design, implementation and development of outputs through a process of engagement between on-the-ground stakeholders, researchers, advisors, etc. around topics that farmers find useful, relevant and necessary rather than a top-down decision from the researcher(s). As it is iterative and intended to foster innovation as well, what will come out of the process is unknown at the start, whereas funders typically require up-front expected deliverables. A change in funding approaches is needed to allow for the autonomy necessary to let this process happen, but it will hinge on policy makers understanding and trusting the process and will likely require the development of new ways to measure, quantify and evaluate impacts to justify expenditure from a public management standpoint.

Multiple breakout sessions were conducted over the four days, highlighting research and projects contributing to four different themes: 1) Education and Extension: roles, functions and tools for boosting interactive approaches to innovation, 2) New skills and capabilities for Extension to achieve innovation policies objectives, 3) Enabling policies for R&I: governance, frameworks and pathways, and 4) The changing role of monitoring and evaluation: approaches, methods and instruments. One of the projects funded under the Horizon 2020 research programme of the European Commission that presented a lot of findings was the AgriDemo project. Researchers talked about the key characteristics and best practical approaches for organising effective on-farm demonstrations identified through the project and how networks amongst the demonstration farms could operate as a support tool for learning. This work is relevant to my PhD research as I work on peer-to-peer learning and farmer engagement within group knowledge exchange events, more particularly farmer discussion groups. I’m conducting participant observation of seven groups over the course of nine months to a year and analysing the data through the lens of social learning theory as understood from an educational psychology point of view in addition to the work around communities of practice, both as applied to farmers and beyond. Thus, the findings not just around how to most effectively structure a public knowledge exchange event to promote farmer interaction and learning that may contribute to practice shifts, but also the limitations of current monitoring and evaluation methods in terms of measuring whether and to what extent learning happened for the participants were very instructive.

The H2020 project LIAISON (Better Rural Innovation: Linking Actors, Instruments and Policies through Networks) also presented its initial conceptual framework now at the start in gathering case study examples throughout Europe of rural innovation in an attempt to identify key characteristics that could be applied to help speed up innovation in other projects and networks. I provide research assistance to the LIAISON project as the University of Exeter is a partner in the 17-member consortium spread across Europe. We are currently in the stage of the project where we are identifying interactive innovation projects and conducting desk-based reviews of their project setup as well as interviews with a project representative to dig deeper into

how the project was specifically designed and implemented utilising participatory approaches with various stakeholders to foster innovation in farm management and/or wider rural innovation. Based on this work where 200 projects across Europe will be profiled in the ‘light-touch review’, a smaller number of projects will be selected on which to conduct in-depth analyses of the core elements that were particularly important in promoting the innovation they fostered and how those elements could be applicable across other projects, regions and objectives to speed up innovation processes.

how the project was specifically designed and implemented utilising participatory approaches with various stakeholders to foster innovation in farm management and/or wider rural innovation. Based on this work where 200 projects across Europe will be profiled in the ‘light-touch review’, a smaller number of projects will be selected on which to conduct in-depth analyses of the core elements that were particularly important in promoting the innovation they fostered and how those elements could be applicable across other projects, regions and objectives to speed up innovation processes.

Finally, I was a co-organiser of the workshop session on ‘Evaluating farmer centred innovation: methodologies and evidence to capture multiple outcomes’, which we ran in the world café style to draw out opportunities, challenges and examples of methods from the session attendees. It targeted the 4th theme mentioned above – The changing role of monitoring and evaluation: approaches, methods and instruments – in relation to farmer-centred innovation as an increasingly popular approach to structuring agricultural interventions, but about which there are critical debates regarding how impact has been or could be demonstrated. This relates again to the issue presented above about funding and the evidence-based results required to justify public investment, but the current evaluation methods are criticised in terms of attributing causation to the intervention when many factors may have played a role in leading to change and thereby overstating impacts. The verifiability and rigorous assessment issues around learning and impact are particularly relevant to my work on farmer discussion group participation in relation to complex decision making and business strategic planning and management for resilience, as farmer knowledge and change in management practices have been monitored and measured, but questions arise as to what indicators could potentially be used in demonstrating capacity development and empowerment. The workshop highlighted many challenges and concerns from a quantitative comparability standpoint (e.g., lack of randomised control trials in measuring the learning process), but the participants also collaboratively brainstormed around possible combinations of evaluation methods that would allow for more in-depth understanding of participants’ internal developments and change through the learning process.

New Project on the Prevalence of Public Support for Conspiracy Theories in Europe

Dr Florian Stoeckel, Lecturer in Politics, University of Exeter

In this new project, we measure the prevalence of conspiratorial thinking in Europe. We also seek to better understand the reasons why citizens believe in conspiracy theories. Joelle Tasker (Exeter BSc student graduating July 2019) and I conduct this analysis based on a novel large-N public opinion survey. The survey was conducted by Kantar Public online. It includes data on conspiratorial thinking in a diverse set of ten European Union (EU) member states and a representative set of about 1100 respondents per country.[1]

Conspiracy theories are usually country specific: for instance, a prominent conspiracy theory in the US is that the September 11 attacks in 2001 were an “inside job” by the US government. A popular conspiracy theory in Poland is about a plane crash in which Lech Kaczyński died. He was president of Poland at the time. One of the conspiracy theories about the crash describes it as an orchestrated assassination. The official investigation identifies errors of the pilots in bad weather as reason for the accident. In our project, we want to make comparisons across countries. Therefore, we use measures that gauge the extent to which citizens believe in political conspiracies more generally, rather than the extent to which they believe a country specific conspiracy theory.

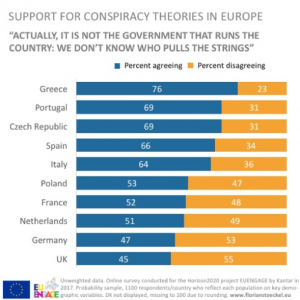

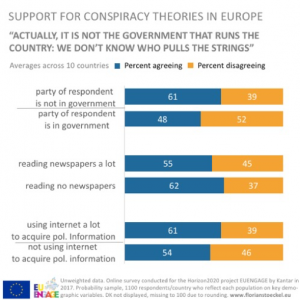

One of our measures for conspiratorial thinking is the extent to which respondents agree with the following statement: “Actually, it is not the government that runs the country: we don’t know who pulls the strings”. We use an individual’s agreement with the statement as one indicator for the presence of conspiratorial thinking. Our preliminary findings reveal much variation between the ten countries in our sample: agreement with this statement ranges from 45 percent in the UK to 76 percent in Greece.

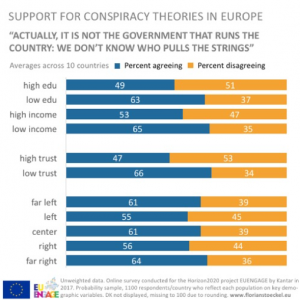

We are also interested in the factors that make it more or less likely for individuals to believe conspiracy theories. Based on a rich literature that examines conspiratorial thinking in the US (e.g. Uscinski and Parent, 2014; Oliver and Wood 2014, Goertzel, 1994), we expect three factors in particular to help us understand who exhibits conspiratorial thinking in Europe. This includes the level of control that individuals perceive to have over their lives, predispositions, and situational triggers. When citizens experience little control over their own lives, they are also more likely to assume that they cannot affect politics either. A conspiracy theory offers a way to rationalise this attitude: it is impossible to affect politics because “we don’t know who pulls the strings” anyway. Experiencing little control over one’s life can be a result of limited material resources, e.g. having a lower income or being involuntarily unemployed. Education, on the other hand, is a cognitive resource which can make it easier for individuals not to feel lost or powerless in a complex political world.

Our survey data support the important role of material circumstances and cognitive resources. On average, the share of respondents who exhibit conspiratorial thinking measured with the above-mentioned survey item is 65 percent among respondents with lower incomes[2] and it is 53 percent among those with higher incomes. The pattern is similar when it comes to cognitive resources. The share of respondents who show conspiratorial thinking among those who did not attend university is 63 percent, but it is only 49 percent among those with the highest levels of education in our sample.

The literature highlights the important role of predispositions for conspiratorial thinking (e.g. Goertzel, 1994; Abalakina-Paap, Stephan, Craig, and Gregory, 1999). We focus on two predispositions: trust and ideological orientations. We are interested in trust as the perception of the world as either a place where one can generally trust other people or a place where one should rather not trust other people. Voters might apply this conception of the world to the realm of politics: citizens who see the world as a place where one can trust other people might be less inclined to think that actors who are unknown to the public are “pulling the strings.” Our preliminary results support this notion. Among individuals who tend not to

An argument from the US context is that conspiratorial thinking is not only a result of characteristics of an individual but that it is also driven by contextual factors. For instance, it makes a difference for voters whether the party they support is in government (Uscinski and Parent, 2014). Voters are less likely to believe in covert agency when their own party is running the country. We find support for this dynamic also in Europe. The share of individuals who say that “we don’t know who pulls the strings” is 48 percent among those whose own party was in government at the time of the survey. The share of respondents who agree with this statement is 61 percent among those respondents whose party was not in government.

Finally, media consumption can be related to the extent to which respondents believe conspiracy theories. We analyse the role of newspaper consumption and news consumption online. We find stark differences: individuals who read newspapers a lot are much less likely to engage in conspiratorial thinking than those who do not read newspapers at all. In contrast, individuals who get their news frequently from online sources are more likely to engage in conspiratorial thinking than those who do not rely on the internet for political news.

trust other people, 66 percent agree with the statement “that it is not the government that runs the country: we don’t know who pulls the strings”. Among respondents who tend to trust other people, the share of individuals who agree with the statement is only 47 percent.

We also examine if left-right ideology is related to conspiratorial thinking, which is an issue that is being discussed vividly in the research literature (e.g. Uscinski and Parent, 2014; van Prooijen, Krouwel, and Pollet, 2015). Our measure for left-right ideology in this analysis is a general left-right self-placement question which does not differentiate between economic issues and cultural issues. We find that the share of individuals who engage in conspiratorial thinking is lowest among those who take a moderate left leaning position or a moderate right leaning position. Conspiratorial thinking is more widespread among individuals who locate themselves at the centre of the left-right dimension, among those with extreme left leaning positions, and it is most prevalent among individuals with extreme right leaning positions.

In sum, we find that conspiratorial thinking is widespread in Europe. The factors that have been identified in an American context also matter in Europe: resources, predispositions, and situational triggers help us to understand the differences between citizens who show conspiratorial thinking and those who do not show conspiratorial thinking. The next step of our analysis includes the development of a more fine-grained instrument to measure conspiratorial thinking and a multivariate analysis of the correlates of conspiratorial thinking.

[1] A household income of 30.000 Euros or less before taxes.

[2] One of the few other comprehensive surveys with a focus on Europe was conducted as part of the project CRASSH at the University of Cambridge. Results can be found here.

Recent Comments